This time every year, VCs and business leaders reflect on the past year and plan for the new year. Our team sat down and discussed our predictions for the next 12 months to inform our strategy and plan for 2024. Needless to say, 2023 was a tumultuous year and 2024 looks to be an exciting year that will require adaptability and flexibility.

Before we made our 2024 predictions, we revisited and graded ourselves on our 2023 predictions, see how we did on our predictions made in last year’s post. The Cervin team is pleased to share our 2024 predictions focused on macro economic and enterprise tech trends that impact us.

Macroeconomic Conditions

While there are still various pockets of weakness in macroeconomic conditions, the technology industry has made a significant comeback. We expect market conditions to continue to improve in 2024 as the cycle of Fed tightening turns. The underlying assumption is that the Middle-East and the Russia-Ukraine conflicts are resolved or contained.

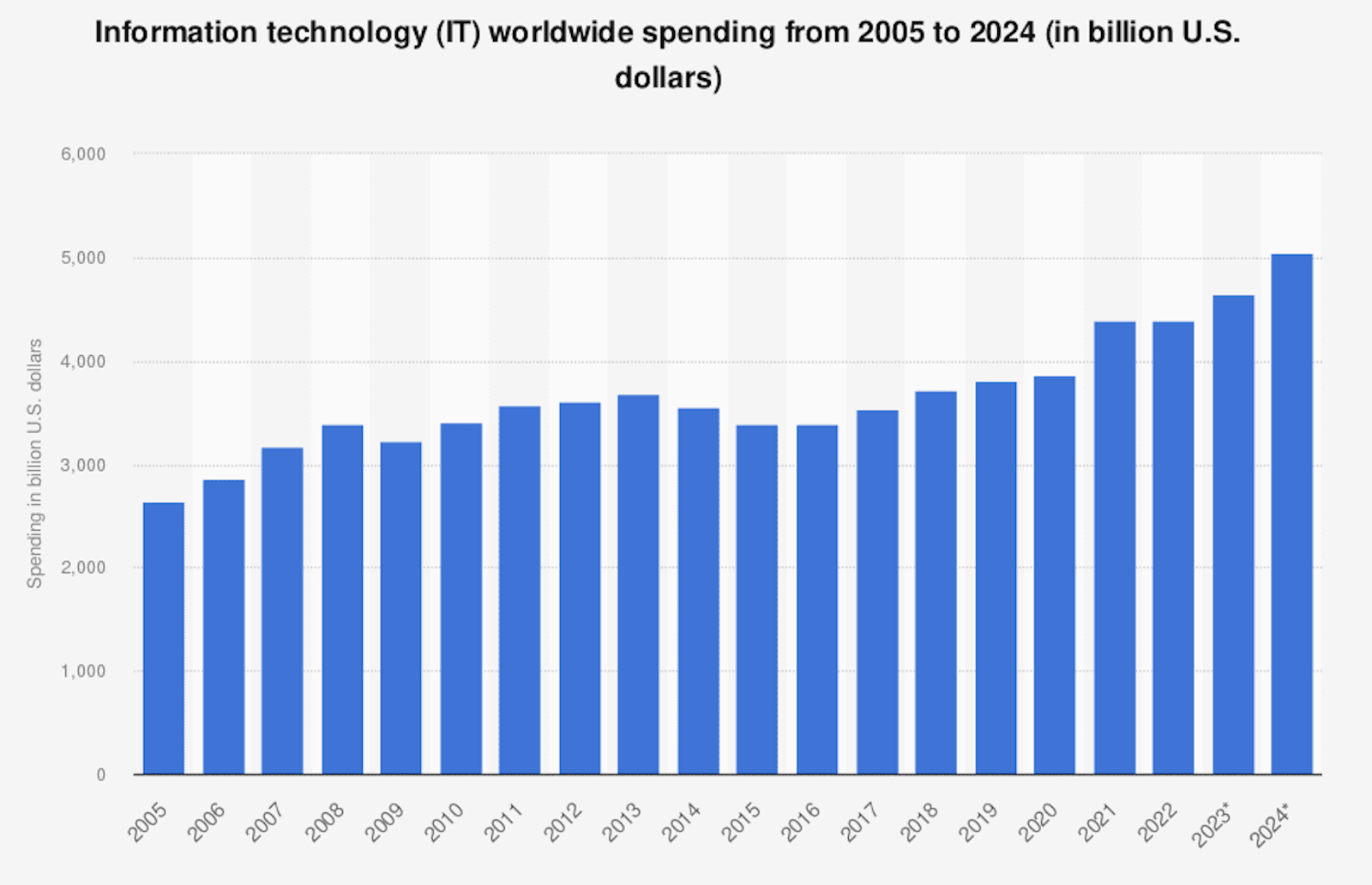

The enterprise IT industry remains healthy and is expected to grow. Gartner expects the entire IT spending budget to increase by 4.7% to $5T (see chart below).

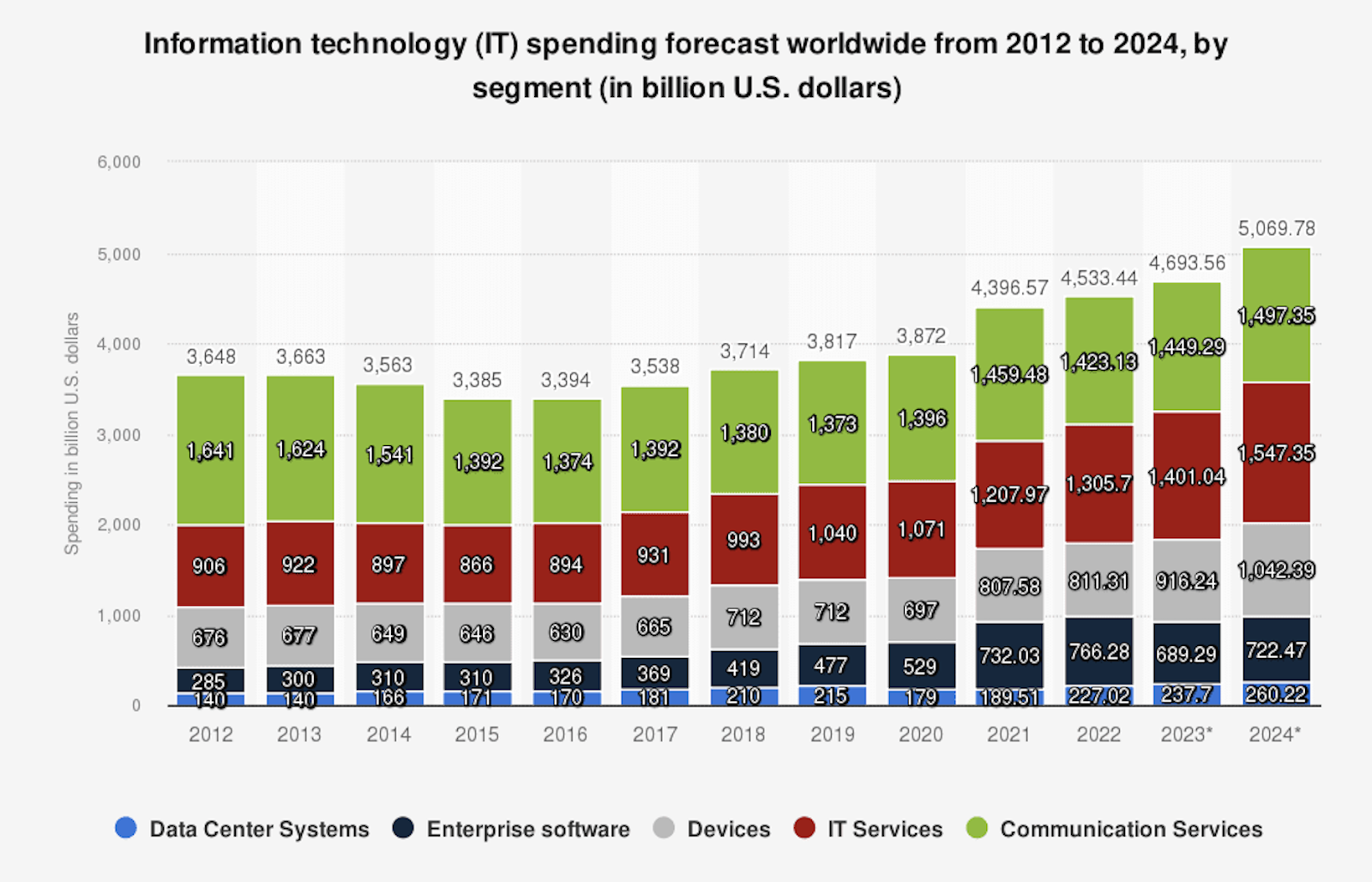

In terms of sectors, IT Services and Communication Services will likely be the biggest areas of spending (see chart below). The enterprise software sector, coincidentally, is expected to grow at exactly the same rate as the entire budget - 4.7%.

State of the VC Market

Despite the hand-wringing in 2023 about venture assets falling out of favor with LPs, we expect US VC funding will go back to pre pandemic levels (~$150B in the US) in 2024. Global trends will follow the US. The venture funding environment will remain strong at the seed stage, but companies raising Series A’s and later will continue to be scrutinized more closely, with continued weakness in Series C and Series D, primarily due to differences in valuation expectations between entrepreneurs and investors. Entrepreneurs will expect valuations much higher than public market multiples justify, while investors will look for guidance at public market multiples. Startups will struggle with balanced growth. Companies will begin to invest in longer-term initiatives such as brand, awareness, events and a high-quality, end-to-end customer experience. Many companies will learn that they cut too deep in certain areas, and 2024 will see heavy investments to rebalance go-to-market motion for B2B startups.

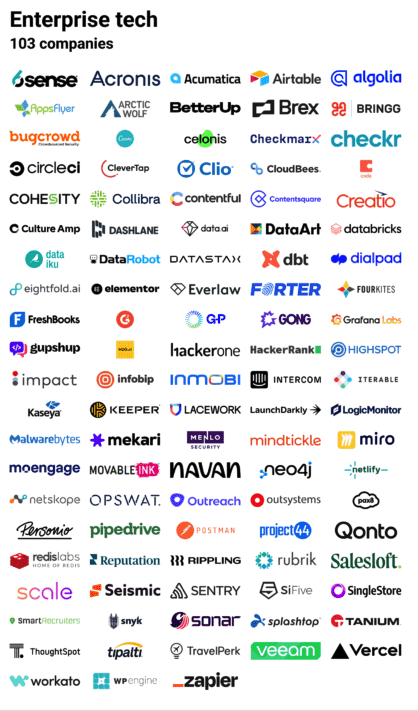

We expect the IPO market to open up in the second half of the year, which will allow traditional growth-stage investing to slowly come back. The chart below shows the Enterprise Tech companies in the IPO pipeline for 2024.

The public market shifted from valuing absolute growth, to valuing profitability, to valuing efficient growth - all this happened in less than 12 months. While it seems, capital efficient growth and models such as the Rule of 40 would drive 2024 operating plans, we expect "operator’s dilemma" of balancing growth vs profitability. There will be a period of time when startups will be operating in the dark with demand and valuation metrics not being very clear. We will see targeted areas where investors will push for growth over profitability as the trend line for interest rates reverses and rates start to come down. Animal spirits may get unleashed but this time around, having been bitten recently, companies will be more careful with use of capital. They still have to grow into the high valuations of 2021-22.

We predict that consolidation in the VC industry will continue. Many funds, whether those who specialized in frothy market segments, as well as ones who haven’t adjusted to a more challenging investment environment, will struggle with managing LPs expectations and with maintaining a steadfast partnership vision and path forward. The glamour of entrepreneurship and VC will wear off. The tourist VCs, the momentum VCs, and executives that left good jobs to start companies for the wrong reasons will start to depart the industry. In the light of a longer J-curve, fewer exits through IPOs or M&A, LP allocations to the VC industry will trend back to pre Covid levels. Many firms will be unable to raise their next funds or raise smaller funds. As the threshold for going public increases, entrepreneurs and VCs with patience and perseverance will succeed. The availability of talent and the scale that AI provides will drive a rise in "foundry-model" and co-creation investments in venture capital. The seed-Bridge/Seed+ ecosystem will have fewer players as fewer companies will be successful in graduating to Series A and B. Those rounds will have higher thresholds as exit options stay limited. Stronger boards, governance and terms will be back in vogue.

On a geographic note, we expect that there will be increased investment activity in LatAm as the next generation has seen the likes of Rappi and Nubank pave the way.